Creating v. Competing

In the not-too-distant past, marketing and advertising were costly and, quite often, labor-intensive (which means “costly”). With social media being readily available and free to everyone, that significantly evened the score for everyone involved. So, instead of having a handful of players who have the money and means to go after a target audience, we now have everybody and their dogs (and cats) going after that same target audience. In other words, the lake remained the same size, but now we’re cheek by jowl full of people casting in their lines and nets to catch a fish.

That doesn’t mean that when Kyle posts “hey if you know someone who is looking to buy or sell a house, let me know” it’s equally effective and persuasive as when Karen creates a multi-media ad featuring pretty people and flashy graphics, but it does mean that both of them are waiting for someone to come to them. In light of this, I recently taught a class to some real estate agents in different ways to create customers rather than marketing to buyers and hoping the buyer will call or email them.

I’m not going to go over the different items we covered (I’m not bitter) mainly because it was a lot of back-and-forth discussion and brainstorming. What I will say, though, is that each and every idea we discussed boiled down to agents and lenders LITERALLY working together to CREATE customers. This doesn’t mean Lender A buys a bunch of leads and sends them over to Realtor B to cull through them and see if any of them are any good. Nor does it mean that Realtor A is going to send out a mailer with Lender B paying for half the costs.

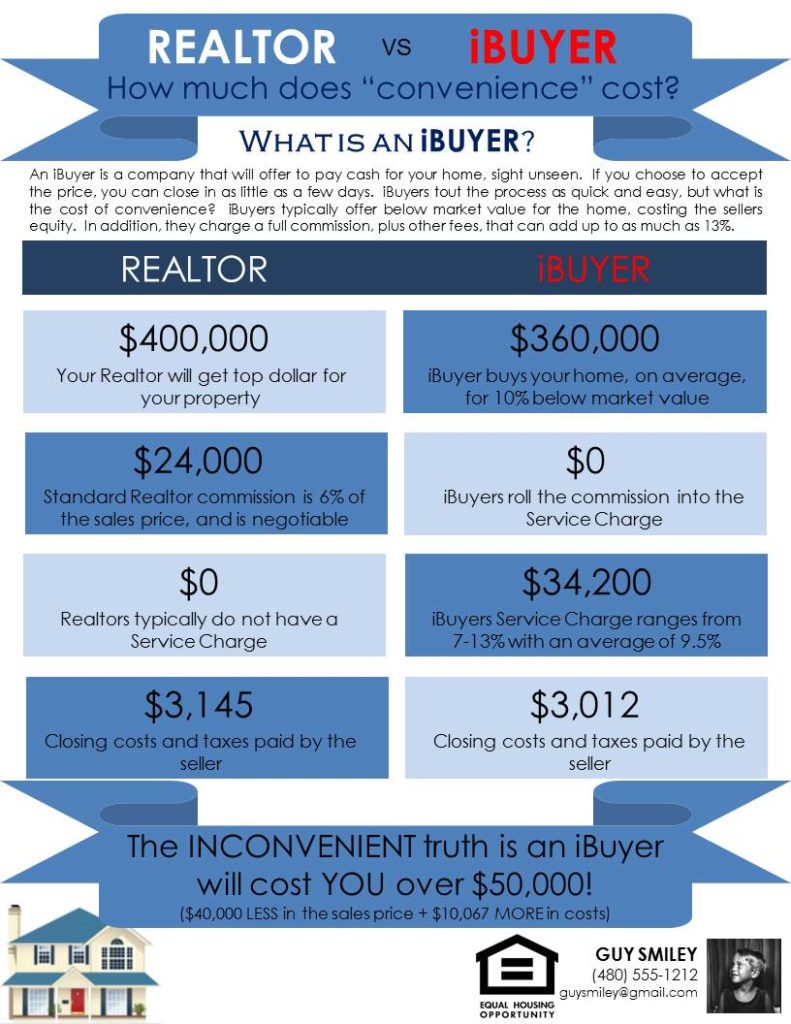

Near the end of our discussion, one of the agents in the class asked that I create a very simple chart that outlined the P&I payment for a certain loan amount in relation to a particular interest rate. For those of you who just rolled their eyes after reading that last sentence, I will agree that such a chart already exists, isn’t that hard to get, and isn’t all that sexy or persuasive. But I will tell you this: it fits perfectly into a plan we had come up with together that will CREATE customers rather than market to people who are already on the hunt for a home (and who every other agent and their menagerie of pets are also trying to attract).

For grins and giggles, I’m including that non-sexy chart. Give me a call if you want me to include your branding on that chart or if you want me to schedule a time to sit down with you and a handful of your fellow agents and go over this brainstorming session on how to create customers. I’m here to help!